The ominous uptick in consumer prices that began in the spring of 2021 triggered alarm bells. By fall, the future looked dark to many observers. A market strategist cited by Reuters warned that the surge in inflation would not be transitory, as the Fed and Biden administration were then promising. “Sticky and sustained” inflation when the country was “past peak growth” would constitute “stagflation," he said, reviving a term coined in the 1960s.

Yet there was no stagflation. The 2021-2022 episode turned out to be very different from the economic turmoil that bedeviled the U.S. economy from the 1960s into the early 1980s. Its brevity was one key difference. A second difference was a far greater volatility of relative prices. A third concerned the role of expectations. As this commentary will explain, these three differences, taken together, carry important lessons for policymakers.

“Transitory” or not, the inflation of 2021-2022 was short-lived

To be sure, not everyone caught stagflation fever. Janet Yellen, the only person to have served as the president's chief economist, Fed chair and Treasury secretary, was one skeptic. “My judgment right now is that the recent inflation that we have seen will be temporary,” she told a congressional committee in May of 2021. By the end of the year, even she had second thoughts. In retrospect, though, her original assessment looks more right than wrong. By the end of 2022, inflation had come down even more quickly than it had risen, and did so while the unemployment rate was, surprisingly, falling.

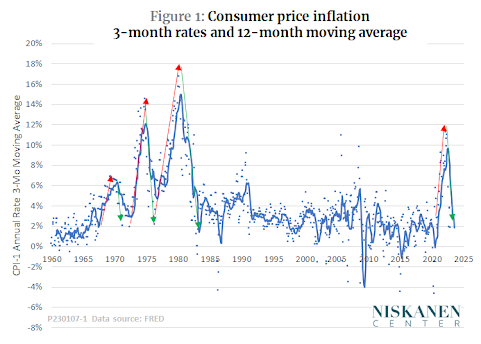

Figure 1 provides a panoramic view of inflation over the past 60 years. The dots show monthly observations, stated as annual percentage rates, for the change in the consumer price index over the preceding three months. (For short, I will refer to these as “3-month rates.”) The solid line is a 12-month moving average of the 3-month rates.

As the chart shows, the wave that peaked early in 1980 was the culmination of three that spanned nearly two decades. Each of the waves made the next one more difficult to handle because of its effects on expectations – a theme to which we return below. The inflation of 2021-22, in contrast, was a single spike that came after a 40-year period of relative price stability that has come to be known as the “Great Moderation.”

Table 1 breaks down the four inflationary episodes into periods of accelerating inflation (shown in the chart by red arrows) and disinflation (green arrows). I count 2 percent per year, the Fed’s target inflation rate, as effective price stability. Accordingly, I measure accelerations from the last month in which 3-month inflation is near 2 percent to the peak 3-month rate, and disinflations from the peak 3-month rate to the month in which inflation drops below 2 percent, or a new acceleration begins. The table also shows the rate of acceleration or disinflation, measured as the number of basis points by which the rate of inflation changed each month. (A basis point is 1/100th of a percentage point.)

As the table shows, the acceleration phase of the 2021-22 inflation was shorter than any of the earlier episodes, and the rate of acceleration, measured in basis points of change per month, was more rapid. The same is true of the disinflation that took place in the second half of 2022 compared to the earlier disinflations – it was shorter in duration and inflation slowed more rapidly.

There has been much debate over whether this episode of inflation was transitory. By comparison with the 1960s and 1970s, I think the term fits, but there is no official definition.

The chart ends in December 2022. Is it possible that inflation will come roaring back in 2023? That 2021-22 was just the first in a series of stagflationary waves like those of the past? The final section will return to that issue, but first we need to look at two other ways in which the recent inflation was different.

Relative prices and why they matter

This section turns to a sometimes-neglected distinction between changes in the average level of prices and changes in relative prices. Figure 1 and Table 1 show only changes in the average price level. Obviously, though, the prices of individual goods and services do not all rise or fall at the same rate. Even while the average is rising, some prices rise more rapidly than others. During disinflations, some prices slow down or even fall while others continue to increase.

Changes in relative prices can be either the result of changes in the average price level, or the cause of such changes.

Consider, first, relative price changes that are caused by inflation – endogenous relative price changes, I will call them. In standard models, inflation is typically driven by changes in aggregate demand, such as those induced by expansionary fiscal or monetary policy. These expansionary policies put upward pressure on prices throughout the economy. However, even if the pressure is uniform, the response to it is not. Some prices change quickly, even by the hour. Others are “sticky.” They change infrequently and only when pressures for change accumulate.

The Atlanta Fed publishes a separate index of sticky prices. According to its research, prices of personal services, public transportation, and rents are among the stickiest, while prices of gasoline, fresh produce, and used cars are among the quickest to move. As a result of differential stickiness, a broad change in aggregate demand induces endogenous changes in relative prices as some markets react faster than others. If overall demand were to stabilize long enough, the sticky prices would eventually catch up. The original configuration of relative prices would then be restored, but at a higher average level.

In other cases, exogenous changes in relative prices are the original impetus for inflation. Suppose, for example, that the world price of oil increases while policies affecting aggregate demand remain unchanged. One might think that as the higher oil price shows up at the gas pump, increased spending on gasoline would divert demand away from other goods, whose prices would fall, leaving average prices unchanged. But in practice, markets don’t work that way.

For one thing, even if demand for goods other than oil falls, prices won’t adjust immediately in markets where they are sticky. Also, oil is not just a consumer good, but also an input into the production of other goods and services. As a result, prices of things like air fares and plastics made from petroleum will rise when the price of oil rises even if higher oil prices divert demand away from those markets. Consequently, the initial exogenous change in the price of oil triggers endogenous relative price changes throughout the world economy.

Episodes of inflation like this that begin with an exogenous change in the price of a single good are known as supply shocks. Supply shocks pose a dilemma for policymakers. When inflation is caused by rising aggregate demand, the Fed’s go-to remedy is to increase interest rates. As the effects spread throughout the economy, they reduce demand for all goods and services, and inflation slows. If rates are raised in a timely fashion and not by too much or too little, the overheated economy will cool off without major disruptions.

Inflation caused by a supply shock is trickier. Since a supply shock begins with an increase in the relative price of one good (oil in our example) and then spreads to other markets where that good is used as an input, there would be no way to prevent an increase in the average price level unless the prices and wages in some other sector fall. But stickiness gets in the way.

Not only are the prices of some goods inherently stickier than others, but many prices are stickier downward than upward. Consider apartment rents, for example. They are sticky even upwards, as we have seen, but even so, landlords will be quicker to raise rents in response to low vacancy rates than to cut rents in response to high vacancies. Wages are especially asymmetrical in their stickiness. Workers are rarely reluctant to accept offered wage increases, but if wages are cut, they protest, fall into an unproductive sulk, or simply quit.

The asymmetrical stickiness of prices and wages is a major problem when the Fed sets out to fight supply-side inflation by repressing aggregate demand. Attempts to offset increases in some prices by pushing prices and wages down elsewhere disrupt markets, raise unemployment, and lower real output. To avoid that, the Fed may prefer to “accommodate” supply shocks by going easy with interest rate increases. Accommodation allows the average price level to rise by enough that even the prices and wages that need to fall in relative terms can do so without actual nominal reductions.

The optimal amount of accommodation depends on just how volatile relative prices are. During the Great Moderation, the Fed settled on a target inflation rate of about 2 percent rather than aiming for zero inflation. That was seen as enough to accommodate the degree of volatility that was then considered normal. However, 2 percent is not necessarily enough to handle really large supply or demand shocks, or both at once.

Coming back from theory to the real world, Figure 2 adds data on the volatility of relative prices (red line, right axis) to the inflation data that was shown in Figure 1 (blue line, left axis).[1] Both variables are charted as 12-month moving averages.

It is clear at a glance that inflation and relative price volatility are related. All four of the major inflation waves discussed in the previous section were associated with increases in relative price volatility. What is more, the deflationary episodes of 2008-2009 and 2014-2015 were also associated with spikes in volatility.[2]

Note, though, that the volatility of relative prices during the 2021-2022 inflation was higher, both absolutely and in relation to the peak inflation rate, than during any of the inflationary episodes of the 1960s or 1970s. The volatility was due in large part to an unusual cluster of shocks, including pandemic-driven shifts in consumer spending from services to goods and back again; supply chain problems that sent prices of new and used cars soaring; and disruptions to world oil and grain markets stemming from the war in Ukraine.

The last section of this commentary will discuss whether or not the fiscal and monetary response to these shocks was appropriate. Before that, however, I would like to point out one more way in which the inflation of 2021-22 differed from those of earlier decades.

Inflation expectations, anchored and adaptive

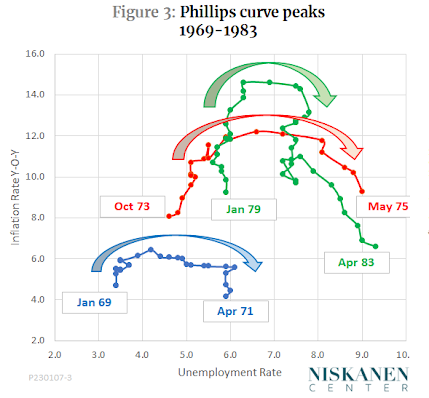

Episodes of inflation and stagflation are often represented using Phillips curve charts. Typically, these show the unemployment rate on the horizontal axis and the year-on-year rate of CPI inflation on the vertical axis. In the traditional version, the Phillips curve is a simple negatively sloped line. Over the course of a cyclical expansion, the unemployment rate falls and inflation rises. The economy slides up and to the left along the Phillips curve. After the cyclical peak is reached, it slides back down along the same path.

In practice, though, the behavior of the economy over the business cycle is not that simple. Figure 3 shows the path of the U.S. economy before and after the inflation peaks of the 1970s and early 1980s. In each case, the unemployment rate began to rise before the peak rate of inflation was attained. After the inflation peak, the unemployment rate continued to rise for several months as inflation slowed. In the chart, that pattern, which gave rise to the term stagflation, forms series of arcs that rise and fall from left to right.

Economists explain the left-to-right arcs in terms of the way monetary policy interacts with inflation expectations.[3] The patterns in Figure 3 were a consequence of the way workers and producers adapted their expectations in the wake of repeated waves of inflation in the 1960s and 1970s.

Here is one way to tell the story: Suppose you are unemployed and looking for work. If a prospective job offers to pay enough to cover not just the rent and grocery bills you are now paying, but the higher bills you expect in the future, you will take it. If not, you will continue looking. Or suppose you are a firm making your production and marketing plans for the coming year. You have plenty of customers, but you expect wages and the prices of inputs to rise, so you ramp up production and raise your own prices preemptively in an effort to preserve your profit margin.

These adaptive behaviors work fine as long as the economy remains strong, but suppose now that the Fed raises interest rates to slow the growth of demand. Workers looking for jobs take longer to find them. That by itself would be enough to raise the unemployment rate. At the same time, firms see sales slow and inventories start to rise. They cut output and lay people off, which further raises unemployment. Yet both workers and firms still expect more inflation to come. Ambitious wage demands and preemptive price increases continue. The economy moves up and to the right along an arc like those in the chart.

Eventually, though, if the Fed sticks to its guns, higher unemployment and slowing demand start to bite. Workers take jobs at wages they would previously have turned down. Firms cut prices to get rid of growing stocks of unsold goods. Inflation slows and the economy moves along the downward slope of the arc. But it takes a long time and a lot of unemployment to finally break the momentum of inflation expectations.

Now turn to Figure 4, which shows the path of the economy in the months around the inflation peak of 2022. Here, the pattern is completely reversed. The arc, instead of running from left to right, runs from right to left. Unemployment falls as the inflation peak approaches, much as posited by the classic Phillips curve. After the peak is reached, inflation rapidly slows with little change in unemployment.

A reasonable explanation of the right-to-left arc in Figure 4 is that this time, inflation expectations were no longer adaptive. Instead, they had become anchored by the decades of price stability during the Great Moderation. That being so, the rising inflation of 2021 and early 2022 did not cause each month’s inflation to be taken as a signal of more inflation to come. Rather, even while the fiscal stimulus from pandemic-era spending, combined with a series of supply shocks, pushed prices upward, workers and firms expected inflation soon to begin falling back toward the Fed’s 2 percent target.

The anchoring of expectations indicated by the 2021-2022 Phillips curve is confirmed by more conventional sources, as Fed Governor Lisa D. Cook noted in a recent speech. After reviewing several measures of inflation expectations derived from surveys and bond market prices, Cook concluded that “expectations are still within their pre-pandemic ranges.”

In short, the available evidence suggests a fundamental regime change from adaptive to anchored inflation expectations over the past 40 years. The change is of more than theoretical interest. Its practical effect has been an enormous reduction in the cost of disinflation. The descents from the inflation peaks of earlier years involved month after month of high and rising unemployment. The descent in 2022 took just half a year, throughout which unemployment remained near historic lows.

Implications for policy

Earlier sections have described three fundamental differences between the inflation of 2021-2022 and the repeated waves of stagflation that roiled the U.S. economy in the 1960s and 1970s.

- Whether we call it “transitory” or not, the recent inflation has been the shortest of the four episodes examined, with the most rapid rate of acceleration and most rapid rate of disinflation.

- The 2021-2022 inflation, which was, in large part, driven by an unusual combination of supply shocks, had the greatest relative price volatility of any period in the last 60 years.

- The decades of the Great Moderation saw a fundamental regime shift away from adaptive and toward anchored expectations, as shown by a reversal of the Phillips curve pattern and confirmed by conventional survey-based and market-based measures.

Here are some conclusions for policy that I draw from these differences.

Policy in 2021-2022 does not look so bad, after all.

Macroeconomic policy over the past two years has had no shortage of critics. Start on the fiscal policy side. In February 2021, when prices were just beginning to rise, Lawrence Summers, a former Treasury secretary and a key adviser to President Barack Obama, weighed in against the size of the economic stimulus package that the Biden administration was proposing. “There is a chance that macroeconomic stimulus on a scale closer to World War II levels than normal recession levels will set off inflationary pressures of a kind we have not seen in a generation,” he said. He pointed specifically to a “risk of inflation expectations rising sharply.”

Monetary policy came in for its share of criticism, too. In a May 2022 interview with CNBC, when inflation had still not peaked, former Fed Chair Ben Bernanke complained of inaction by monetary policymakers. “Why did they delay their response? I think in retrospect, yes, it was a mistake. And I think they agree it was a mistake,” he added.

Yet, from the perspective of early 2023, the past two years of monetary and fiscal policy look much better. Yes, inflation in mid-2022 spiked to its highest levels in four decades. Yes, many people felt the pain. But would a tighter budget and higher interest rates imposed earlier really have eased that pain, or only changed the form it took?

Shutting down the growth of aggregate demand in early 2021 would not have erased supply shocks from the pandemic, war, and tangled supply chains. But slower growth of demand would have made it more difficult to achieve the necessary relative price realignments. With slower inflation, unavoidable relative price changes would have required actual cuts to nominal prices and wages in lagging sectors, rather than just relatively slow rates of increase. I have been calling that “asymmetrical price stickiness,” which is a rather bloodless term, but it reflects a real psychological aversion by firms to resist price cuts and workers to resist wage cuts. Forcing those cuts would have meant lost jobs, personal and business bankruptcies, and loan defaults. Paradoxically, even though the peak rate of inflation might have been lower, the recovery would likely have been slower and accompanied by higher unemployment rates than what we actually saw in the second half of 2022.

Writing for the Financial Times, Raghuram Rajan, himself a former central bank head, laments how difficult it is for central bankers to establish the right kind of credibility. Should they focus entirely on establishing a reputation as fierce inflation fighters? Or should they let it be known they will accommodate higher inflation when appropriate? Rajan thinks the Fed played it too loose in 2021-2022. I think that whether by strategy or purely by luck, they got it just about right.

The Fed needs to pay more attention to relative prices.

This commentary has highlighted the role of supply shocks and relative price changes in the 2021-2022 inflation. Fed officials are beginning to pay attention, too. In the presentation cited earlier, Fed Governor Cook includes a chart showing the dramatic divergence in inflation rates in three key sectors of the economy. She asks, “Would adopting a model with multiple price components improve our understanding of and ability to forecast overall inflation? Relatedly, should we look to inflation models with nonlinear or threshold effects?” My answers are, “Yes, and yes!” Relative price changes, both endogenous and exogenous, should be central to the Fed’s planning, not an afterthought. So too should the nonlinearities introduced by differential and asymmetrical price stickiness.

{kind=link}

Neel Kashkari, president of the Minneapolis Fed, is another high official who is catching on to this. In a recent essay, he criticizes the Fed’s “traditional Phillips-curve models,” which consist of labor market effects via unemployment gaps, changes to long-run inflation expectations, and little more. These “workhorse models,” he says, “seem ill-equipped to handle a fundamentally different source of inflation” which he describes as “surge pricing inflation” – his own term for one kind of the relative price effects discussed here.

“Can we,” asks Kashkari, “develop frameworks and tools to analyze and potentially forecast inflation outside of the labor market and expectations channels?” He answers himself in the affirmative. “If we can deepen our analytical capabilities surrounding other sources and channels of inflation, then we might be able to incorporate whatever lessons we learn into our policy framework going forward.”

A suitable model might start with a multi-sector input-output framework to trace the impacts that price increases in one sector, such as energy goods, has on others, from farming to freight transportation to plastics. A dynamic version of such a model could incorporate differential and asymmetric price and wage stickiness as price shocks are passed from one sector to another. By gaming out different monetary policy strategies, such a dynamic, nonlinear, asymmetric model could estimate the optimal degree of monetary accommodation in the face of various kinds of endogenous and exogenous shocks. I am far from having either the analytical firepower or the data needed to construct such a model, but the Fed, with its vast resources and hyper-talented staff, surely does.

Get ready for the post-moderation world.

It would be wonderful if we could breathe a sigh of relief that we got through the COVID-19 exit crisis with only a transitory bump in inflation, and could now look forward to renewal of the Great Moderation. But that isn’t going to happen.

For a laundry list of the shocks ahead, we can turn to the great Gloom Meister himself, Nouriel Roubini. Writing in December for Project Syndicate, Roubini listed five “wars” that cloud the economic future: hot or cold wars between the West and revisionist powers; a war against climate change and its effects; wars against pandemics and the demographic effects of aging populations; wars against disruptions from artificial intelligence and other new technologies; and wars against rising inequalities of income and wealth. As the wars themselves eat into output and desperate governments try to inflate their way out of unsustainable debt, Roubini sees the outcome as – you guessed it – global stagflation.

I’m not quite so pessimistic. In the short run, in the United States, the greater risk is likely to be a plain old recession without the inflation. Christina Romer, head of the Council of Economic Advisers in the Obama administration, explained why in a 2022 keynote address to the American Economic Association. The problem, which she illustrated vividly with a pair of charts, is that any policy moves by the Fed take about two years to affect output and unemployment. That means that sharp increases in interest rates since 2021 are just now becoming visible. Because of the long lags, says Romer, “policymakers are going to need to dial back before the problem is completely solved if they want to get inflation down without causing more pain than necessary.” A “soft landing” without recession is still possible, but the longer the Feds sticks to its strict anti-inflation program, the less likely that becomes.

Neither is 1970s-style stagflation in the cards in the longer term, at least not in the United States. The only way to get true stagflation would be to run both monetary and fiscal policy flat out for a decade or more, long enough to break the inflation expectations anchor. The Fed may make some mistakes, but nothing that big. If it gets busy and updates its models, based both on what has gone wrong and what has gone right in the past two years, there are real grounds to hope that the pessimists will be proved wrong again.

Originally published by Niskanen Center, Jan. 30, 2023. Reposted by permission.

[1] There seems to be no generally accepted metric for the volatility of relative prices. In Figure 2, I use monthly values of the standard deviation of rolling 3-month inflation rates across 11 CPI components: Energy goods, energy services, transportation services, new vehicles, used vehicles, food at home, food away from home, apparel, medical services, medical goods, and shelter. Those 11 account for about 80 percent of the CPI.

[2] Economists are taught not to trust their eyes alone. Let V be the monthly value for the measure of price volatility. Let A be the monthly “inflation anomaly,” that is, the absolute value for a given month of the difference between the 3-month inflation rate and the average inflation rate over the preceding two years. The correlation of P with A is positive and statistically significant (R = 0.54).

[3] See this earlier commentary for a more detailed explanation of the theory behind the next few paragraphs.

No comments:

Post a Comment