As talk of a new recession grows louder, everyone is

watching some favorite indicator. The yield curve, claims for unemployment, the

quits rate — you name it. What surprises me is how few people are watching an

underappreciated indicator from the New York Fed that uses more than just price

data to tell us what is happening with inflation.

As talk of a new recession grows louder, everyone is

watching some favorite indicator. The yield curve, claims for unemployment, the

quits rate — you name it. What surprises me is how few people are watching an

underappreciated indicator from the New York Fed that uses more than just price

data to tell us what is happening with inflation.

What makes the Underlying Inflation Gauge (UIG) unique is

its power to distinguish between changes in the cost of living and changes in

the rate of inflation. Did you think those were the same thing? Think again,

and read on.

What’s the difference?

The concept of the cost-of-living stems from the first of

those role of money as a medium of exchange. When we say the cost

of living increases, we mean that it gets harder to maintain a given standard

of living on a given income. Either we have to be satisfied with fewer goods or

services, or save less, or work harder. In the language of economics, a change

in the cost of living is a real phenomenon.

Inflation, in concept, is best understood a change in the

value of our unit of account, the dollar. When there is inflation,

the value of the unit is smaller each day than it was the day before, for all

transactions.

Imagine that you woke up one morning to find that someone

had chopped an inch off all our rulers, so that today’s foot was now only as

long as yesterday’s eleven inches. You might go from being six feet tall to

six-foot-six, but it wouldn’t be any easier for you to reach the top shelf in

the kitchen without a footstool. Similarly, if inflation raises both your

income and the prices of everything you buy by the same percentage, the value

of a dollar as an economic ruler shrinks, but it is neither harder nor easier

to maintain the same real standard of living. In that sense, inflation does not

measure anything real. It is a purely nominal phenomenon.

There are two other important differences between inflation

and changes in the cost of living.

First, although they are both harmful, they are harmful in

different ways. An increase in the cost of living hurts people because it makes

them poorer. The harm from inflation is more subtle. Inflation makes it harder

to plan for the future, so it discourages investment. It erodes the real value

of cash and other assets that have fixed nominal values, so it discourages

saving. Because the rate of inflation typically becomes more variable as it

becomes more rapid, it increases uncertainty. People can overcome some of the

uncertainty by indexing the contracts they make, but indexing is costly and

never perfect. When we take all these effects together, inflation makes markets

work less efficiently and slows economic growth.

Second, the effects of inflation are the same for everyone,

but changes in the cost of living vary from place to place and from person to

person. If inflation shrinks the unit of account by 3 percent, then the real

values of anything with a fixed nominal value — a paycheck, of a Treasury bond,

or of a contract to deliver goods — all fall by 3 percent. In contrast, a

change in a broad index like the consumer price index (CPI) affects people’s

cost of living differently according to which components change. An increase in

the price of heating fuel affects people in cold regions more than those in

warm regions. An increase in the price of meat does no harm to vegetarians. The

cost of living in New York does not necessarily keep pace with that in Oklahoma

City.

Can we measure inflation and the cost of living

separately?

The CPI is primarily a measure of the cost of living. Each

month, the BLS gathers data on the prices of hundreds of goods and services.

After making adjustments for changes in package sizes, and, periodically, for

changes in quality, it reports the result as a weighted average. If your

consumption patterns are reasonably close to the average, the change in the CPI

tells you how much harder or easier it is to maintain your standard of living

on a given nominal income.

We can take the CPI at face value as a measure of the cost

of living, but we have to do some work to extract information from it about the

rate of inflation.

A good first step is to adjust the CPI for predictable

seasonal changes in the cost of particular goods. For example, everyone knows

that the price of fresh vegetables goes up when the summer harvest season is

over, but if we expect the price to go down by the same amount next summer, we

don’t count the seasonal change as inflation. Consequently, the BLS reports the

monthly CPI in both a seasonally adjusted version and a version without

seasonal adjustment. Adjusting the raw CPI for predictable seasonal changes

greatly smooths month-to-month volatility. We can also get rid of seasonal

variations by looking at the CPI for any given month compared to its value 12

months earlier.

Another way to extract an inflation signal from the noise of

month-to-month changes in the CPI is to sort out price changes that have

particular, microeconomic causes from those that have more general,

macroeconomic causes. Microeconomic causes include things like extreme weather

events, wars, or developments in global commodity markets. Macroeconomic causes

include changes in monetary policy, changes in fiscal policy, and the state of the

business cycle.

Food and energy prices are particularly susceptible to

transient microeconomic events. To sift them out, the Bureau of Labor

Statistics publishes a so-called core CPI, which

removes the food and energy components. As the following chart shows, the core

CPI is considerably less volatile than the CPI itself, even when the CPI is

averaged over 12 months, so it gives us a better idea of the underlying rate of

inflation.

An even better way to measure inflation

But, economists at the New York Fed think there is an even

better way to measure inflation. Instead of removing data from

the CPI to get rid of the noise, as the core CPI does, why not add data

to get more information on underlying trends in the unit of account? The

additional data used by the New York Fed includes real variables, like

employment and output data; monetary data like trends in the money stock; and

financial data like interest rates and bank credit. Subjecting all of this data

to a complex filtering procedure gives the Underlying

Inflation Gauge. The New York Fed supplies monthly values for the UIG going back to 1995.

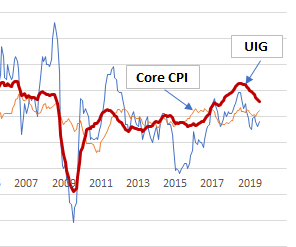

Here is what we get when we put the three inflation series

together:

First, we see that the UIG, like the core CPI, tends to

smooth the data. It is not as volatile as the CPI itself, but it is a little

more volatile than the core CPI. That already tells us that it has some value

in filtering out the inflation signal from the cost-of-living noise.

More importantly, though, the UIG is much more sensitive to

cyclical variations in the economy. Although the UIG only goes back far enough

to capture two previous recessions, what it shows us is highly suggestive.

In June 2000, the rate of change of the UIG began a

sustained decrease some nine months before the start of the short recession

that began in March of 2001. The UIG continued to slow throughout the

recession. In contrast, the rate of inflation as measured by the CPI remained

high and more volatile during the recession, and the rate of increase in the

core CPI actually rose.

A similar pattern can be seen going into the much deeper

Great Recession that began in December 2007 and lasted until mid-2009. The rate

of change of the UIG began to slip well before the recession started, and fell

steadily once it was well under way. In contrast, inflation as measured by the

CPI itself increased in the early months of the recession, and the rate of

change of the core CPI was actually higher a year after the onset of the

recession than when it began.

The bottom line

A word of caution: The above is only “eyeball econometrics.”

We don’t have a long enough data series for the UIG to give statistically

conclusive results. But, with that disclaimer in mind, if you’re looking for

early warning signs of an impending recession, I’d keep my eye on the UIG

rather than either of the other two measures of price trends.

The UIG has been falling for 10 months now. True, it gave a

false alarm with a similar decline starting in mid-2011, but this time the

downturn in the UIG coincides with other worrying trends in world trade and

financial markets. It just might mean something.

Previously posted at Medium.com

No comments:

Post a Comment